Blog 2. International Stock Exchange and Stock Market Efficiency

Gan Kian Siong ID No: 14045693

Introduction of World stock exchange

Based on World Federation Exchange (WFE), it represents 63 regulated exchanges over 46 thousand listed companies, across all major stock exchanges in various continents, (table 1). World stock exchanges factions all across the globe, have become one of the major regulated institutions. It is a marketplace for traders and brokers to trade stocks and securities in the financial markets. Total trading volume around 65% of world GDP are considered, these enormous figures play a direct role in the making and crashing of the world economy.

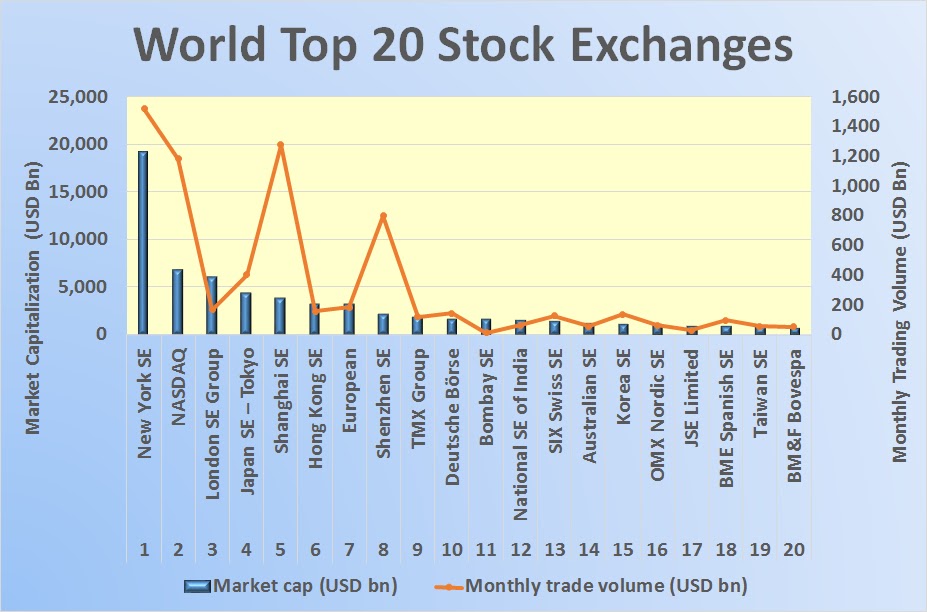

Table 1. Source: World Federation Exchange, 2015. Top 20 major stock exchange of the world

According to the World Federation Exchange, 2015, (table 2). Top 20 major stocks exchanges in the globe resided a total of US$ 64.2 trillion (market capitalization). A total trading value of USD 111 trillion or USD 9.25 trillion (average monthly) trading volumes, of which top 20 exchanges represents 80% of the world stock exchange were traded across countries to countries.

Based on JP Morgan report, the global market capitalization weights in MSCI, all countries world index and the share of global GDP in 2015. (Table 3) Shown United States (46%), Europe (16%), Emerging Market, include China (13%), Japan (8%), Pacific or others (5%) and Canada (4%). For the share of Global GDP, the emerging market stands out top 50% follow by the United States (19%) and Europe, exclude-UK (17%).

Table 3. Source: JP Morgan January 2016. Weight in MSCI all-country world Index

Based on FT report in 2012, (table 4) the emerging markets have contributed vastly to the growth in both stock market value and in listings. The exchanges at the bottom center left cluster (highlighted in red rectangular shape) saw fast growth in market capitalization associated with a decline in listed companies. The bubble size = USD 1 trillion which is proportionate to the market capitalization (Financial Times, 2012)

Table 4: Source: Financial Times, World Federation of Exchanges, (WFE) 2012

The causes and effects of advance in global financial markets

Globalization era

Globalization era evolves in the recent decades has accelerated in the foothold since the 1970s, this tenure is used to designate the relationships between communities and states, how they were created by the geographical spread of ideas at both local and regional levels. Literally, these phenomena process accelerate the integration of trades, and therefore, the expansion of industrial globalization, international trades, and modern financial markets have been increasing substantially (Rugman & Collinson, 2012). The effect, however, leads to stern competition has led corporations and market leaders to expand its off-shore business such as increasing M&A activities, in order to compete in the world marketplace. These creations provide new opportunities for both industrialized and developing countries. The largest impact has been in developing countries, who now are able to attract foreign direct investment (FDI) and foreign capital and this has led to both positive and negative effects for those countries (Financial Times, 2012).

Deregulation Factors

The aim of deregulation is the removal of local and central government oversight the industry, market, and economy. It is implemented with the intention of creating competition within an industry (Lumpkin, 2009). The effects allow businesses to improve trades, increased labor, reduce or lower cost of capital, easy access to fund and capital mobility, capitalize advance technological know-how and entry to new market penetrations etc.

A classic example, during the phase of Big Bang era, a sudden deregulation of financial markets in the UK, with the austerity measures had to put in place, the London SE had shifted from an open outcry to electronic screen-based trading, the effects by Margaret Thatcher on October 27, 1986. The same day the London SE was dubbed the "Big Bang" due to the increase in market activity. The effect of the Big Bang led to significant changes to the structure of the financial markets in London. The changes saw many of the old firms being taken over by large banks both foreign and domestic (City of London's Policy and Resources Committee, 2006). These deregulations had occurred in Singapore in 1999, the MAS introduced the policy to liberalize foreign access to Singapore's domestic banking market. As the banking industry is further liberalized, local banks over the years have merged to fortify against foreign competitions (Lee & Phoon, 2014).

Financial Innovation Effects

Since it is started from a premise that financial innovations are a natural outcome of a competitive economy. Financial Innovations have the potential to provide a more efficient allocation of resources, and thereby a higher level of capital productivity and economic growth. For example, many innovations prove to be beneficial from the digital electronics net base, but some others result in an adverse and severe outcome, as innovations can affect financial intermediation, and the effective working of the financial intermediation process is essentially a matter of public interest (Lumpkin, 2009) .

Efficient Market Hypothesis (EMH)

There are three types of efficiency market hypothesis and it rhetoric concerned with the ascertain production and distribution with the assumed resources (Arnold, 2013).

Productive efficiency

This occurs when the maximum number of goods and services are produced, with a given amount of inputs to produce maximum output for the minimum cost. These may draw market competition and reflect at a normal market price or narrow profit margin is inevitable.

Allocative efficiency

The effectiveness of the markets is therefore in its distribution of capital to the maximum productive. A market with high allocation efficiency will eventually provide the essential capital to industries with business opportunity for growth........................................................

…………………………………......

Pricing efficiency

An investor can expect to capitalize a calculated risk-adjusted return from a stock investment, velocity price movement constantly moves reflected according to the market news.

Random Walks appears relative to the S&P 500

According to Goldman Sachs report in July 2015, several years of emerging market (EM) underperformance – relative to the S&P 500 and developed international equities are alike – have left investors with shrunken EM allocations (Goldman Sachs, 2016), (table 5). A random walk theory occurs when the share price at any one time reflects all available market information and it will only change new information arise. Successive price changes will be independent and price follows a random walk due to the next piece of news releases. Investors could not be able to predict correctly if any information is relevant or is it going to be good or bad. Therefore, market news releases, the share price moves to its new rational and equitable level (Arnold, 2013).

Table 5. Source: Bloomberg, GSAM and Goldman Sachs, July 2016

Information Announcements: Market Reaction and Efficiency Theory

During the 70s, Eugene Fama, had distinguished the relationship of three form of EMH, the market reaction to the efficiency theory. As an example how efficient market response and co-relates to FCA NV share price (monthly chart) and Yahoo share price (five years’) chart (Table 6). The share price instantaneously adjusts to the new level high. And literally, price corrected back to the efficient market level that was similar charted as shown below.

Line 1. Slow Reaction – Market take a longer period to absorb a consolidation phase of various moving average lines shown in the chart until the share price approaches the new efficient level.

Line 2. Anticipatory price movements – Base on recent earning performance, the market could anticipate the new announcement. Share price begins to rise before the official announcement.

Line 3. Overreaction - Followed by price correction due to market overreactions to the information and causing vast sell down, some institutions will take advantage to short the stock price of a particular stock or future index.

Line 4. Persistent inefficiency – Once the market price is corrected, the shares may continue to be unpriced for a considerable period due to a support level, the investor will then could take a fresh position given the market with a lower discounted price.

Table 6: Source: Yahoo Finance.com, Yahoo 5 years’ stock price trend.

References

1. Arnold, G. (2012). Modern Financial Market And Institutions. Financial Times.

2. Arnold, G. (2013). Corporate Finance Management.

3. City of London's Policy and Resources Committee. (2006). Big Bang 2 years on New Challenges facing the Financial Services Sector.

4. Financial Times. (2012, August 20). Chart of the Week: The Listings Race of Emerging Markets.

5. Goldman Sach. (2016, July). A Return to a Lower, More Variable Trend for Equities.

6. Lee, D., & Phoon, K. (2014, July). Singapore's Financial Market: Challenges and Future Prospects. Singapore Managment Univeristy.

7. Lumpkin, S. (2009, December). Regulatory Issues Related To Financial Innovation. OECD, 2.

8. Rugman, A., & Collinson, S. (2012). International Business (Sixth ed.). Pearson.

No comments:

Post a Comment